Instead of getting tough with servicers, Treasury says they work with banks to make sure problems are fixed.

When government audits of banks’ modification practices revealed they were frequently breaking the rules, Treasury officials worked through a process they call “remediation.”

One audit, conducted on Treasury’s behalf by the government-supported mortgage company Freddie Mac, found that 200,000 struggling homeowners had not been told they were eligible for the program, as servicers are required to do. Auditors also found 15 of the largest 20 participating servicers were incorrectly using the Treasury formula that determines if homeowners qualify for the program.

Rather than imposing penalties, Treasury simply asked the servicers to contact the homeowners that had been missed and rerun the numbers for those who had been wrongfully denied because of the formula error.

“The servicer says, ‘you’ve caught me this time,’ but it doesn’t improve widespread non-compliance because there’s no real penalty,” said Alys Cohen of the National Consumer Law Center.

Dawn Patterson, Treasury’s chief of compliance for the program, explained that the idea was to allow servicers time to get “their programs built, their processes more shored up.” Patterson says Treasury is continuing to use that approach.

The most common complaint is that the servicer has violated the program’s guidelines.

Complaints to Hotline Increasing

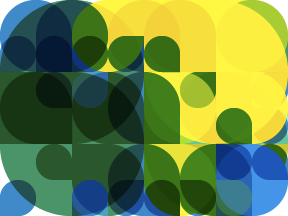

10.3%6.1%Nov. 2010March 2010

This data, obtained through a Freedom of Information Act request, comes from the HOPE Hotline, a help line for homeowners sponsored by the Treasury Department. Complaints are calculated as a percentage of total calls, excluding irrelevant calls like hang-ups and wrong numbers.

Servicers have also at times been uncooperative with the government’s own auditors. Even getting the right documents from servicers has “been a cumbersome process,” the head of the government’s audit team, Paul Heran, said last year at an industry conference. It seemed, he added, the task was often relegated to low-level staff who didn’t understand the requests. Another manager in the unit, Vic O’Laughlen, said servicers tended to respond with “at best fifty percent of what we’re expecting to see.”

A Treasury spokeswoman said that “servicer operations, especially in larger organizations, are complex,” and producing the documents can be difficult.

The government’s oversight has also been hampered by a lack of transparency by Treasury itself. The department has kept its audits of servicers secret. It also does not have a written policy for how it would address rule violations by banks, an omission criticized in a Government Accountability Office report last year and not yet addressed. Treasury says it does have a process for dealing with banks’ noncompliance, just not a written one.

The lack of oversight has been particularly damaging, since mortgage servicers have little incentive to do modifications on their own.

Servicers handle homeowner payments for investors who own the loans. Since servicers don’t own the vast majority of the loans they service, they don’t take the loss if a home goes to foreclosure, making them reluctant to make the investments necessary to fulfill their obligations to help homeowners.

“By every metric, the failure of the largest servicers to carry out the program is obvious,” said Prof. White. The noncompliance has gone unpunished, he said, because “Treasury staff are preoccupied with friendly relations with the banks. Sometimes it seems the banks own Treasury.”

Meanwhile, the industry has continued to lobby for changes in the program.

Last summer, Treasury significantly weakened a tool that would have helped keep servicers accountable after officials met with industry lobbyists, documents show.

When banks entered the program, they agreed to certify annually that they’ve followed the rules of the program. But lobbyists from the Financial Services Roundtable and the Mortgage Bankers Association suggested adding exemptions.

Instead of certifying that banks had followed all the rules, the industry proposed that they could ignore problems affecting less than five percent of homeowners eligible for the program. In the case of Bank of America, which handles more mortgages than any other bank, that meant the bank would not have to report an error that occurred nearly 20,000 times.

The industry also suggested that no matter how widespread a problem, servicers could assert they were complying with the law as long as they pledged to fix problems “to the extent practicable.” The previously unreported proposal was disclosed through an administration policy of releasing lobbying contacts related to the TARP.

Later that month, the Treasury revised its certification requirements, making them similar to those the industry sought. Under the new rules, servicers can define for themselves what violations were significant enough to disclose.

The new policy is “not only like putting the fox in charge of the hen house,” said Cohen of the National Consumer Law Center, “but asking the fox to fine itself for each chicken eaten.”

A Treasury Department spokeswoman said the industry’s lobbying did not affect the final guidance, because Treasury was already going to make several of the servicers’ suggested changes. It was never the department’s intention that “a servicer submit a list of every individual instance of non-compliance.” If servicers give themselves inappropriate leeway, she said, Treasury would work with them to address the problem.

Unless servicers fear real penalties, the troubled program is unlikely to improve, said Richard Neiman, New York state’s chief bank regulator. “There needs to be a greater effort on enforcement, on assigning sanction and fines where there has been noncompliance. We cannot rely solely on servicers to police themselves.”

RELY on SERVICERS?? Are they kidding?? Chase is by far, the WORST, and I say this because I’ve been battling with them for over 2 years. NOW, they’re telling me, “since the gov. is the investor for your FHA loan, we DO NOT review for a HAMP/FHA-HAMP unless you don’t get approved for the REGULAR FHA modification, which, of course is OUR very own Chase CHAMP.”

So, let me get this straight – FHA REGULAR mod. IS the Chase CHAMP, which is laden with erroneous (to coin Chase Relationship Mgr. Carol Masters’ favorite term) fees, interest, “anticipated foreclosure fees,” etc. Now, you have to remember, this story changes every time I speak with someone from the sacred Exec.Offices somewhere in Chase-ville.

Unreal. Letting servicers police themselves is like telling my 4th graders to follow our every day routine if I’m absent. It’s like telling kids to make sure they let me know if they cheat on a test. COME ON !!!!! Really??????

Just to add to my earlier post, the Treasury is afraid of what the servicers will do if they impose strict & REAL consequences??? THIS is the reason WHY the banks know they can get away with what they’re pulling. Behavioral Psych 101. WHO is in control???? The parent or the child??? Who NEEDS to be in control – no brainer.

Real numbers of complaints to the Hotline are probably even higher. I called to complain but they basically refused to take my complaint and steered me into yet another financial counselor call.

Delighted to see more groundbreaking investigative journalism from ProPublica. Remarkable, astute, concise and sophisticated work here.

If this f.c. crisis was not leading to a new American diaspora, larger than that of the (first) Depression, it would be bitterly funny.

But I am not laughing. I am wondering why none of this was not mentioned by the President, who likes to refer to our “recovering” economy.

Atrocious malfeasance by well-paid Feds, whose salaries, benefits and pensions are drawn on hard-working taxpayer contributions.

Livid to realize that these turkeys work for me. Their cow-towing to banks, esp. the astounding behavior of Phyllis Caldwell, is a true affront to taxpayers.

After 14 months We have finally received a trial payment schedule. starting 3-1-11 our mortgage will be $208 lower. is it low enough? wait and see.

I never gave up and pressed BoA hard! they offered a forbearance ( no payments for 3 months ), but thats not what I asked for, nor was it the program I applied to. So, i just set that paper work aside because no one at BoA would return my phone calls about it.

If in the end they try to foreclose on me I plan on filing for bankruptcy and claiming lack of support from the government program, and the banks unwillingness to perform to the program.

Please do not lose hope. i recieved a permanant loan mod from Wells Fargo over 4 monthes ago. It does happen, do not give up! They reduced me from 6.5% to 2.75%. This saves me $560.22 every month. Stay in your program, keep sending in your same documentation over and over. Send it every 30 days, even if they don’t ask for it. Get their fax number and fax them updates of your bank account statment every month. This shows reliability. Often, the people you talk to on the phone are low level personel who are trained to get people frustrated, so they will give up. Ask to talk to your final processor about every 3 months or so. If you have not been assigned one yet, ask to have your application reviewed by the dept. that assigns clearance for forwarding to a proccessor. Above all, do not lose your temper with anyone you speak to, this is sure to get an error introduced to your app that will delay it at best, and kill it at the worst. Good luck all, Mike Survell

How much longer can the banks get away with this? I have seen people go to prison for stealing a pack of cigarettes yet the bank can steal people’s homes and it is okay?? When will the Government step in and place a freeze on these foreclosures and make them fix this S***! Also for the other people that actually did lose their homes how can there not be repercussions. The Government and the banks are the only people in the USA that never get punished!! Oh and Homeowners Associations. Doesn’t anyone see how large this is!!!! I live in Chicago and went to start meditations because that is the 1st step and honestly it was standing room only for six hrs. Grown men were reduced to tears. There were people with homes ranging from 700,000.00 to 50,000.00. All I heard was they just wanted a chance to make things right and why we were all being made to go through the process over and over!!! I asked the housing counselor how often they see this injustice and she replied every hour of every day. I asked about paperwork and she replied I am sure it is in a pile beside someone’s desk waiting for the shredder. In Chicago the people involved in the housing crisis are volunteers. The mediation lawyers are overwhelmed and quitting daily. Some quitting just for the fact that they can not look at themselves in the mirror because they can’t fight the foreclosure lawyers who also do not know what they are doing because they too are overwhelmed. When Bank of America got wind that I opted for mediation because they denied my one and only modification for incomplete financial paperwork I received a letter stating they really want to work with me please feel free to call. They have been trying to contact me but were unable to!!! So they type up a 3 page letter stating they will do everything possible to help me. We’ll maybe because I am trying to work during the hrs they call and they never leave a message?? Some days I just don’t want to get out of bed!!! But I have to I have child to take care of!!

Be Blessed everyone and lets keep fighting!!!

Servicers lie with impunity.

Servicers deny loan modification applications with impunity.

Servicers manipulate homeowners into paying partial payments through temporary modifications while they continue the parallel process of foreclosure.

Servicers lie with impunity.

I believe it is a myth that the servicers were granting modifications at first without proof of income. Show me this data. I have never seen it.

Servicers lie with impunity.

Timothy Geithner has said that MHA was created to spread out the foreclosures for the benefit of the banks. Main Street is on its own, with a few exceptions like ProPublica. Thank you.

I have also battled with citibank for 2 years and they have done all sorts of manipulating with my account including not responding to inquiries and not posting payments on my account since may 2010. They then torpedoed a forebearance plan my way that was not credited properly and now a trial payment plan. What makes it worse is because of the mess up in accounting and numerous credit inquiries by citibank I’m finding it almost impossible to refinance with anyone else.

For almost 2 years, I have been trying to get into the HAMP program, I have now completed 3 trial payments. On January 5, I was told that the “FED EX” package would be sent out within 7-14 business days for me to review and sign.

CHASE LIES (big surprise.) I call them almost everyday, and I speak with the same representative as I have her direct extension. She claims that my file is still in “Review” review of what? NOTHING they are just stalling.

CHASE Bank is nothing more than a group of lying scumbags that spend millions on lobbyists so that they can continue there bulls**t.

Our government needs to grow a set, and get tough with the banks. Why did they agree to give the banks all this money? Henry Paulson should be shot.

@ Michael Survell – many of us have been offered the 2% interest rate. The issue is that this leaves the nut intact, a monster to wrestle with another time. My home will never regain the mtg. amount (let alone the down payment that is lost.)

The 2% deals just kick the can down the road. Many people would be better off considering a f.c.and a fresh start than hanging onto a house that one way or another will be impossible to sell for what is owed.

TOO BIG TO FAIL? THE BANKS PROTECT THEIR ASS ettes by buying off the politicos. Barter with your neighbor! The system is set up to benefit the exploiter.

If you are in none-judicial state be prepared to be served with a Fraudulent Notice of Default.

Fraudulent Notice of Defaults are the new Robo-Signing era. And guess what, so far banksters getting away with it and repossessing homes.

This housing mess will never be cleaned up by voluntary actions from the banks. It is sad that banks in America have more power then the people and the Government.

Thomas Jefferson was right.

I believe that banking institutions are more dangerous to our liberties than standing armies. If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around [the banks] will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.

Thomas Jefferson,

3rd president of US (1743 – 1826)

SO WAKE UP AMERICA AND DO SOMETHING ABOUT THESE BANKS.

THERE ARE INDIVIDUALS OUT THERE WHO HAVE NO PROBLEMS WITH BANKS TODAY.

BUT SOONER OR LATER THEY WILL

Until Director Walsh is replaced at OCC, nothing will happen. He is in the pocket of the banks. Just watch his testimony before congress. He is a weasel.

OCC does not investigate like they are supposed to. All they do is forward your complaint to the bank. THEN if YOU get an unsatisfactory response – they will FOLLOW UP.

They also told me not to follow up with them, as that is a waste of their time.

I am at 16 months with dealing with Chase and Deutsche Bank, Chase is just a bunch of liars and cheats who no intention of following rules or doing a mod for anyone. BUT, neither of them can prove title here in KS, so we will see.

Yes there are lots of ways for crooks to get the better of us and do it without shame or care. Its hard to have confidense in our government leaders who looks like they are letting guys get away with this stuff. Howcan we trust anybody surly not our leaders or congressman. This is disgusting to read over and over about bad people getting it over the regular guy on the street and families workin to get buy.

They will sell my house for half of what I owe rather than give me a principe reduction after 30years with a sick 90 year old mother and a husband who had a stroke over them. Go figure.! The Banks are Evil and are “The Mafia without a Gun”! I never thought when I worked so hard for Obama and Jerry Brown I would lose my house ! “Stupid Me” Good name for a movie!

Hi everyone, it’s been awhile since I’ve been here. I was wondering if anyone ever had any luck with a law suit? Also Chase ruined our credit by reporting us late each month, they have refused to ammend this on our credit report. Has anyone had the same thing and if so, we’re you able to get Chase or any other bank to contact the credit bureaus? Please let me know.

Thanks!!!

Kim

I work at a HUD approved housing counseling agency. Those servicers will use any excuse to deny a loan modification. Most often, its been my experience they simply (intentionally?) use wrong numbers for the NPV test. Additionally, I quite often am forced to speak with a customer service person who is untrained and totally without knowledge about the loan modification program. Here is an example: Yesterday we were on the phone with BofA asking yet again for the inputs on a specific NPV evaluation. The customer service person from BofA told me that BofA does not do its own NPV test but that it has Treasury do the test for them. The BofA representative told me to go to the Treasury webpage and click on the icon for NPV results. I played along and said ok, I’m at the Treasury web page, where’s the icon? The BofA representative hung up on me. How ridulous is that?

Excellent coverage here… thank you Pro-Publica for keeping on this story… confirming what so many have suspected all along!

WAKE UP AMERICA, YOU’VE BEEN SCAMMED AGAIN.

Trial period/foreclosure fees, etc,etc,etc.

Wake up America, you’ve been scammed once again by the Banksters, who are the US Treasury Dept.

Trial period/foreclosure fees, etc,etc,etc.

I work at a HUD approved housing counseling agency. In Orange County, CA we no longer let the servicers get away with refusing loan modifications. We advise our homeowners who were wrongly denied a loan modification to file a lawsuit. All foreclosure lawsuits are assigned to the same judge and the judge sets a loan modification mediation. At the mediation a HUD approved housing counseling agency is present along with the homeowner and the judge. The judge asks the housing counselor if the homeowner qualifies for a loan modification. If the housing counselor responds “yes”, the judge asks the servicer why they are refusing to give the homeowner a loan modification. The servicer is also reminded that they are to negotiate in good faith. If the Judge does not like the response he sometimes orders a continuance and orders the servicer to bring someone with authority to the next hearing. We are seeing at these hearing that many times the servicer used the wrong numbers when they ran the NPV test. It has been my experience that servicers usually short the homeowners monthly income by a few thousand a month and then deny the loan modification. The beauty of this court program is that the program has teeth. The servicers are held accountable. The program is getting loan modifications for OC homeowners. The program has now spread to the Federal Court as well. The servicers do not like the Program and in the past have removed the lawsuits to Federal Court. However, the Federal Court started the same program so the servicers are having to face housing counselors in Federal Court as well. I hate to have to advise homeowners to file a lawsuit, but for many homeowners its either get foreclosed out or save your home by filing a lawsuit.

I am a victim of BOA and the so called “making home affordable” modification program!! I have just made my 20th trial period payment in A 3 MONTH TRIAL PERIOD, for MHA modification. Every month since I started paying (May 2009-Current), I request info and status updates and have always been told, “your still in the review process” and to “keep making your trial payments”!! It is so convoluted and upsetting that every time you call its nothing but run around and each of these so called representatives knows nothing about our file, or what the other hundreds of reps have told us before!! They accept my payment EVERY month, but can offer me NO information of the finality of my modification!! This January 2011, when I called to make my 20th payment, I was horrified when I was told(after many transfers to different departments) that i was “declined from the MHA back in July 2010, because of “lack of financials”!!!! How come I was never notified in writing nor in any of the many calls in the previous months when I would make my payments!!!!! How absurd, they actually told me they sent a FedEx, THAT I NEVER RECEIVED, and when I asked if someone signed for this so called FedEx, I was told, “they just drop it off, without a signature”. It is nothing but a rat race, with no end. Now as of February 10th, they are going to begin foreclosure proceedings, when I NEVER defaulted on one single modification trial period payment, NOR WAS I EVER INFORMED OF SUCH A DECLINE from the program. The amount now due to be current is so exorbitant, I could never, never pay that amount. They have put in another so called “escalation email to appeal the decline”, but lets be real, nothing is going to be done!!! I risk foreclosure now, when I had all intentions on fighting for my home, by paying for almost 2 years in a modification program which I now feel DOES NOT EVEN EXIST!!!!!!!!!!!!!!!!!!

All these experts reporting on and stating the lack of oversight, broken promises, violations, etc, BUT NOBODY DOES ANYTHING!!!!! All the government agencies we pay for thru our taxes, will not even respond to written complaints. The Treasury Secretary and Jamie Dimon of Chase are VERY CLOSE FRIENDS! Of course, Treasury isn’t going to do anything. We need Class Action Suits, we need lawyers to conduct them, we need Attorneys General to file suit against these banks. We, The People, means nothing anymore. We are lied to by our government, ignored by our elected representatives, but expected to pay, pay, pay.

What good is reporting all the grievances, if it doesn’t result in any action??

During the financial crisis over the last three years, nobody has taken real ownership to help the public. The govt has bailed out the financial corporations that started this mess; govt has passed laws without any teeth; politicians keep on talking hot air; corporations keep on thumbing their noses and lining their pockets; and the public keeps on getting the short end… and people wonder why there is voting apathy and distrust of govt!

There is a good bit of information at this blogspot about what to do about the banks/servicers trying to impose a fake mortgage debt that does not exist on all of us. I received this tip from 4closurefraud.org though ProPublica’s website deserves a ton of credit to for their spot on reporting on the Foreclosuregate Crisis that raised my suspicions about the deceptions behind the whole loan mod program and began my journey looking for the truth behind all of the lies and deceptions. Here is the blogspot with Homeowner’s Motto for 2011:MODIFY,BUT ALSO NULLIFY!: http://bryllaw.blogspot.com/2011/01/homeowners-motto-for-2011-modify-but.html

“The new policy is “not only like putting the fox in charge of the hen house,” said Cohen of the National Consumer Law Center, “but asking the fox to fine itself for each chicken eaten.”

Exactly!

Until the banks are actually put in the position of loosing money they will do nothing for the consumer. I think the answer is to stop the f.d.i.c. from covering the banks losses in the foreclosure fiasco thereby forcing the banks to negotiate with homeowners. And please, no one post another “homeowners bought more than they can pay for stories”. and how no one should be helping them out.

We need to stand together as Americans and STOP PAYING these crooks (ie:banks). If the majority of us do it they will be crippled and they will have to DO something. DO NOT PAY any trial period payments without the advise of an attorney and everything in writing. DO NOT PAY if you owe more than your home is worth. Here in Florida that is everybody (almost). The banks ran the prices up (with the help of realtors) and they CAN NOT POSSIBLY take back all the homes in the state. Tell everyone you know STOP PAYING, worst case scenario you will live for free for 2 years, which will get some of your equity back and then move on or modify legally and DO NOT ACCEPT a huge balloon payment at the end just cuz you are so grateful to the thieving banks that they temporarily lowered your payment. You are then just postponing the inevitable. I have met with 3 independant lawers and they all said the same thing (STOP PAYING). If WE ALL STOP PAYING WE ARE IN CHARGE. They have treated us like suckers for years let it end NOW. Know that is is starting: my friend paid $450K for a beautiful house a mile from the beach, she has been trying to modify for 30 months, to no avail. The bank just had an auction for it with a stop/loss of $110K and NOBODY BID!!!! No one wants a Florida house (sorry don’t know much about other states). There is too much inventory (1500 forclosures in my zip code according to Realtytrack) Prices are not done falling. STOP PAYING and force the scum banks to fall, WE ARE THE ONES WHO BAILED THEM OUT!!!!

We have been trying to get Chase to help us for 2 years….not asking for a handout, just a break!! They have come up with every excuse in the book, so I am just going to let God take care of all of their greedy selves in his time!! Life is too short!! We make to much for Loan Mod, too little for refinance, and supposedly don’t qualify for the Freddie Mac no qualify refinance, because our loan has 2 investors, which it doesn’t. It is owned by Freddie Mac & serviced by Chase. They even made up a new word “refrapricated???”, and the majority of the supervisors don’t know what it means!! Obama needs to get in the real world. This is the biggest “joke” against the American people I have ever seen!! Keep up the great work!!

What do you expect from banking industry exec’s who make all policy decisions for the gutless lower end woking lawyers to follow their directions no matter how one sided industry oriented.

What else would you expect from oversite by politico’s dependent on industry money and then appoint them to high positions and set the policy for the enforcement. If it looks like a duck >>>>>!

Last year, I finally gave up, abandoned my home of more than 20 years, and moved into my travel trailer. What the banks are doing, they’re doing because they’re being allowed to do it.

The officers and board of directors at Chase and the other major lenders should be stripped of their wealth and imprisoned for their part in defrauding the American people. Millions of homes are now in foreclosure.

What do the lenders do with this glut of homes? They put them out on short sales, then collect their taxpayer-funded insurance from Treasury. Meanwhile, the short sales depress the legitimate market even further. If there was any real interest in resolving the problem, the homeowners who are losing their homes would be allowed to repurchase them at short sale prices, then provide mortgages at affordable interest rates.

Will any of those things happen? Unlikely!

Maureen, wait until crybaby Jamie reads the following report – which essentially demonstrates that these banksters all had plenty of warning signs, and concludes it was avoidable.

Earlier today the Financial Crisis Commission released their report which can be viewed and downloaded from their website at FCIC dot gov. You can also view many of the thousands of docs they used to compile the data. I’ve only just begun….

A snippet from the conclusions of the commission (pg xv):

“As this report goes to print, there are more than 26 million Americans who are out of work, cannot find full-time work, or have given up looking for work. About four million families have lost their homes to foreclosure and another four and a half million have slipped into the foreclosure process or are seriously behind on their mortgage payments. Nearly $11 trillion in household wealth has vanished, with retirement accounts and life savings swept away. Businesses, large and small, have felt the sting of a deep recession. There is much anger about what has transpired, and justiiably so. Many people who abided by all the rules now find themselves out of work and uncertain about their future prospects. The collateral damage of this crisis has been real people and real communities. The impacts of this crisis are likely to be felt for a generation. And the nation faces no easy path to renewed economic strength.”

Last year, we finally gave up, abandoned our home of more than 20 years, and moved into our 15 year old travel trailer. What the banks are doing, they’re doing because they’re being allowed to do it.

The officers anddirectors at Chase and the other major lenders should be stripped of their wealth and imprisoned for their part in defrauding the American people. And make no mistake about it: what has happened has been deliberate.

Millions of homes are now in foreclosure.

What do the lenders do with this glut of homes? They put them out on short sales, then collect their taxpayer-funded insurance from Treasury for the difference. Meanwhile, the short sales depress the legitimate market even further. If there was any real interest in resolving the problem, homeowners losing their homes would be allowed to repurchase them at short sale prices, then be provided mortgages at affordable interest rates.

Will any of those things happen? Unlikely, considering there’s no incentive for the banks to do so.

Can homeowners use the Findings from the recently released Report of the Angelides Commission? These Findings are based on real EVIDENCE of lenders’ fraud.

It is true there is a dissent to the Report. The dissent frankly proves that the Commission with its public hearings and large number of experienced witnesses and participants gave them every opportunity to present their case. They failed.

Of particular interest is the “dissenter” who dissented from the other dissenters. Representative Wallison is an interesting Boehner appointment to the Commission. He is the lawyer who helped author the “deregulation of financial services” that eventually became law in 1999. Now, Wallison is blaming the 40 million homeowners who manipulated the equity in their homes and cheated those poor bankers who were finally provided the opportunity to pillage their own institutions. Does it make sense to blame homeowners who were subjected to intense marketing of OptionARM terms that even the bankers cannot calculate?

Look who Wallison is:

# 1981-1985 General Counsel for the Department of the Treasury, under Don Regan. He was important in developing Reagan administration proposals to deregulate financial services that, with some changes, became law in 1999.

# 1999–present American Enterprise Institute, codirector of AEI’s financial markets deregulation project. He is a paid lobbyist/ sitting Congressman.

He is a PAID apologist for the Financial Industry that destroyed itself, billed the tax payers, gave themselves bonuses, and now blame everyone else. His dissent contains interesting attacks on “Government”, as if the idea was invented two years ago by some Democrats. Just attacks and speculations, no real facts.

LISA!! Please go check out being middle class dot org website. There are dozens of letters and guidelines for you to follow there, not to mention countless other victims of every bankster imaginable, all in various stages of this horrendous nightmare, and ALL willing to share their experiences, write letters, direct you to Escalations teams, and support you in every way!

I too have been scheduled for a sale next month (my third one!) after Chase sent me an official denial letter for a permanent mod based on failing their NPV results after being in the program over a year. HOWEVER, same letter gives me 30 days to review their NPV and another 30 to dispute their results, and even states “Important Notice!” that they will not foreclose on me during this time! HAHAHAHA!!!!! Today, they posted the sale notice on my front door and I received the notices in the mail from California Reconveyance of my sale date of Feb 18th! Guess I better tell them again to re-read the terms of the letter they sent me!

Should you pay your Morgage? Of course. Unless it is a fraud—such as an OptionARM. If a banker lured you into a financial arrangement that was inappropriate, and defrauded you with a term that makes it impossible to calculate your obligation, and then defrauded you and the Government by falsely promising to provide a Loan Modification, then you should re-think any obligation to pay.

Legally and morally you have no obligation to pay installments to gangsters.

If you cannot afford to hire your own licensed real estate attorney, at the very least, please report the financial institution to the State Bar. If the corporation hires non-attorneys to practice law, they are violating the law in every State. Unlicensed practice of law by corporations is illegal.

Any HUD Counselor or anyone advising a homeowner how to save the Lender money by entering into a short sale or deed in lieu, is “advising you about your legal obligations”. Many of those people are scammers or were trained by the Lending Industry to protect them.

It is only reasonable to stop paying gangsters. Report them to the authorities.

This month, the long-awaited US House Committee on the Financial Crisis (a bipartizan investigation chaired by Rep Phil Angelides) issued its Findings. Those “Findings” are a form of evidence, and the evidence justifies recovery of damages for Fraud. Use those Findings in your “negotiations” with the attorney for the Lender.

And again, if the Lender is not negotiating with a licensed attorney, then report them to the State Bar.

This is an OUTRAGE! Thank you for this important journalistic investigation. Shame on all responsible for continued violations or deceptions. May I suggest that everyone move money from the bad banks to those not tainted? Perhaps that is the only leverage the American people have left.

Jean – thank you for the info on that report!!! Poor Jamie. See? I told you guys what goes around comes around. SOmetimes it just takes longer than we’d like.

Although I’m not doing the “yippee dance” yet, I have a good feeling we will be soon. I’m one of the lucky ones with a stable job – Thank God – but they STILL won’t offer me anything more than the dreaded Chase CHAMP (I wrote the latest development – if that’s what you could call it – on BMC – it sounds like a sitcom). According to the “new rep. on the block,” “FHA loans are invested in by the gov. (no way!! really??) so they won’t allow us to review for a HAMP or FHA-HAMP first because our Chase CHAMP is the REGULAR FHA mod.” Not buying it.

fantastic coverage by ProPublica… all bright, informed

What I for one as a tax payer would like to know is where did the 75 Billion provided by the current administration go, you know money provided by hard working Americans. From what I read here it has been sent down a rabbit hole of no return and accountability. Was this then just a back door bailout of the “servicers” who have been able to string hard strapped homeowners on only to end up in foreclosure!

Where did 75 BILLION go? And who benefitted, apparently not the struggling homeowner!

“With millions of homeowners still struggling to stay in their homes, the Obama administration’s $75 billion foreclosure prevention program has been weakened, perhaps fatally, by lax oversight and a posture of cooperation—rather than enforcement—with the nation’s biggest banks. Those banks, Bank of America, Wells Fargo, JPMorgan Chase, and Citibank, service the majority of mortgages.”

Pastor Dave is right, they collect the insurance for the loss in forclosing and then resell (or not) at auction. If they sell it’s icing (money on top) as they have already collected, fully funded by you and I thank you very much. It is legal robbery, STOP PAYING!!! THAT is why they won’t modify, they don’t make as much. STOP PAYING THE ROBBERS FORCE THEM TO THIER KNEES!

Anyone who has seen what I have written on various articles here knows that I have been skeptical of the government’s role in this thing. But I guess I always told myself maybe I was just into it on too personal a level to be objective and maybe I was crying FIRE where there wasn’t one.

But I can see now, and I take no joy in it, ProPublica which has stood with us throughout this ongoing tragedy, has come to the same conclusion as I have or else I have come to the same conclusion as they.

The facts are what I have been stating all along, we have been sold a bogus bill of goods.

The taxpayers and citizens and voters of the U.S. were told that we were bailing out these “too-big to fail” institutions of money grubbers but that they were in return going to have to adhere to and follow rules and regulations and help a lot of people in return. The facts don’t back that up.

As ProPublica has stated, the government has been insincere from the beginning and as bad as it is to feel like you’ve been “had” by a business, to feel you’ve been “had” and lied to by your “trusted representatives” is a major blow to my trust in anything my government says or does.

How do we decide when/if they give us the truth. We now have to suspect everything we are told which is wrong. We should have trust in our government, we are entitled to a government that is worthy of trust but the facts say that ain’t the way it is.

This is a shocking realization to me and it makes me very sad and very concerned too. What other lies are up their sleeves to tell us next? When they swear that things like 9/11 and Waco were honestly disclosed, that we know the truth about Tim McVeigh and Oklahoma City, how now do we trust them when they are proven liars? The answer is, if you are smart and willing to look at facts however scary they are, is WE CAN’T.

Tracey,

Maybe CHASE won’t do so well now that the guy responsible for their lobbyists, William Daley, has left the company for another job.

Oh, wait a minute; his new job is Whitehouse Chief of Staff!

Never mind.

Pat in your comment Today, 4:09 p.m Can you please elaborate more? who file this kind of law suit and how?

I ll appreciate the info

My email sassonn@sbcglobal.net

July 09 we recieved a supposed permanent loan modification from BofA. Made my payments on time every month. Had my credit report pulled 9 months later and found that I was 9 months behind on loan! Started making multiple phone calls daily, finally a month later told ” it was not funded”! And I was given no further information no matter how many calls I had made. Finally after writing letters to my senators, congressmen, governor… I received a phone call from the customer service CEO’s office. They told me that there was an error in the escrow calculations in my batch of loan modifications and they took it back and had sent me a new loan modification! Never got one phone call, letter or paper work on new loan modification. And the thousands of times I called not one of those horrible customer service reps told me anything of this error, they told me to keep making the modified payment and that the system had not been updated. So now we are being reviewed for another loan mod, but they are adding in all the remainders of what they say are the partial payments we were making and late fees! Unbelievable! At my wit’s end don’t know what to do to get this fixed!

So glad to know that they are finally being exposed for all of there wrong doings and hope that they get caught for all that they have done to ruin peoples lifes.

Come on everyone this is not new Bank of America Became the richest bank in the world by foreclosing on the Japanese Americans land and homes while they were in relocation Camps remember “Manzanar

Iwould not be in this position if my father in law could have left me our inheritance . Banks have not changed! Maybe we have had enough!!!!! But they have always been there. Doing the same stuff we were working and did not have time to notice.

The whole program needs to stop now! Let the banks take all the properties, then nobody buy them.Take all the bailout money back and redistribute it those who lost their properties perhaps that would really shake up the banks.

The HAMP prgram shoul be call the Making Home Delaying Foreclosure Program This program was made only to delay foreclosures while the Banksters Stick you up with Inspection Fees, Interest, Late Fees and most of all the payments you make while in a trail a period, those payments are not being apply to your mortgage nor being return to you either they keept them in a suspend account and then when the foreclose they keep them ROBING YOU of your money

HAMP= License to rob you!

God Bless America !